Liverpool Unit Market: From 3% Growth To A Perfect Storm

Selling a unit in Liverpool? – Here are some numbers you should know

At the beginning of 2026, we were fairly confident. The forecasts were modest but optimistic: 1–3% growth in unit prices across the Liverpool LGA. We’d analysed the data, looked at the trends, and figured we had a reasonable handle on where the market was headed. Geez, were we wrong.

We didn’t expect a declaration of war on investors with the recent capital gains tax changes. We didn’t anticipate the inflation needle would move as much as it has. And we certainly didn’t factor in the impact of increased petrol prices on buyer sentiment and investment returns. Add to that the RBA’s continued rate hikes and you’ve got yourself a perfect storm – the kind that catches even experienced market watchers off guard.

Today, just six months into 2026, the Liverpool unit market looks nothing like what we predicted. And if you’ve got the stomach for it, just visit realestate.com.au and scroll through the pages of units for sale in Liverpool and Warwick Farm. What you’ll see tells a story that the headlines haven’t quite caught up with yet.

So what’s actually happening? That’s the big question. And given that my position of 1–3% growth forecast is now shot down in flames, you should probably take my six-month prediction with a grain of salt – or better yet, throw it over your shoulder. But the data is real, the trends are clear, and the story it tells is worth understanding.

THE PERFECT STORM: FOUR FACTORS CONVERGING AT ONCE

Let’s be honest about what’s happened in the first half of 2026. This isn’t just about interest rates or housing supply. We’re dealing with a convergence of factors that have created a genuinely difficult environment for unit investors and buyers.

- The Capital Gains Tax Bombshell

The proposed changes to the capital gains tax discount haven’t even become law yet, and they’re already having a measurable impact on the market. As Greg Jericho noted in his recent analysis, the CGT discount – which has been in place since 1999 – has been ground zero of the housing affordability crisis. Now that the government is finally addressing it, investors are panicking.

The data is striking: nationally, dwelling prices have fallen around $100,000, or roughly 10% year-on-year. In Sydney and Melbourne, we’re seeing 7-8% declines. That’s not a gentle correction – that’s a market recalibration. And it’s happening because investors are reassessing their portfolios in light of CGT changes that will reduce the discount from 50% to 25% for assets held longer than a year.

What does this mean for Liverpool? It means investor demand has softened considerably. Properties that would have attracted multiple investor bids six months ago are now sitting on the market longer, and sellers are being forced to adjust their expectations.

- Inflation Refusing to Play Ball

We thought inflation was under control. The RBA thought inflation was under control. Turns out, inflation had other ideas. The needle has moved more than expected, and it’s forcing the RBA to hold rates steady at 4.35% – and potentially hike further.

Higher inflation means higher mortgage servicing costs for buyers who are already stretched. It means rental yields are being compressed because rents aren’t rising as fast as property prices fell. And it means the “investment case” for units has become considerably weaker than it was twelve months ago.

- Petrol Prices and the Cost of Living Squeeze

We don’t often talk about petrol prices in the context of property markets, but we should. When petrol prices spike, it affects buyer sentiment in ways that aren’t always obvious. People have less discretionary income. They’re more cautious about taking on debt. They’re rethinking whether now is really the time to buy.

In Liverpool and Warwick Farm, where many buyers are first-time purchasers or investors with limited capital buffers, petrol price increases hit harder than they do in wealthier suburbs. It’s a squeeze on the margin that pushes some buyers out of the market entirely.

- The RBA’s Hawkish Stance

The Reserve Bank has hiked rates three times in 2026 and is explicitly keeping the door open for further increases. The board’s June statement made it clear: they will “do what it considers necessary to achieve” price stability, “including increasing the cash rate target further if required.”

Translation: rates could go higher. And every time the RBA raises rates, it pushes more marginal buyers out of the market. In a suburb like Warwick Farm, where the median asking price is $475,000, a 0.25% rate rise can mean an extra $30-40 per week in mortgage repayments. For buyers on tight budgets, that’s the difference between being able to afford a property and being priced out entirely.

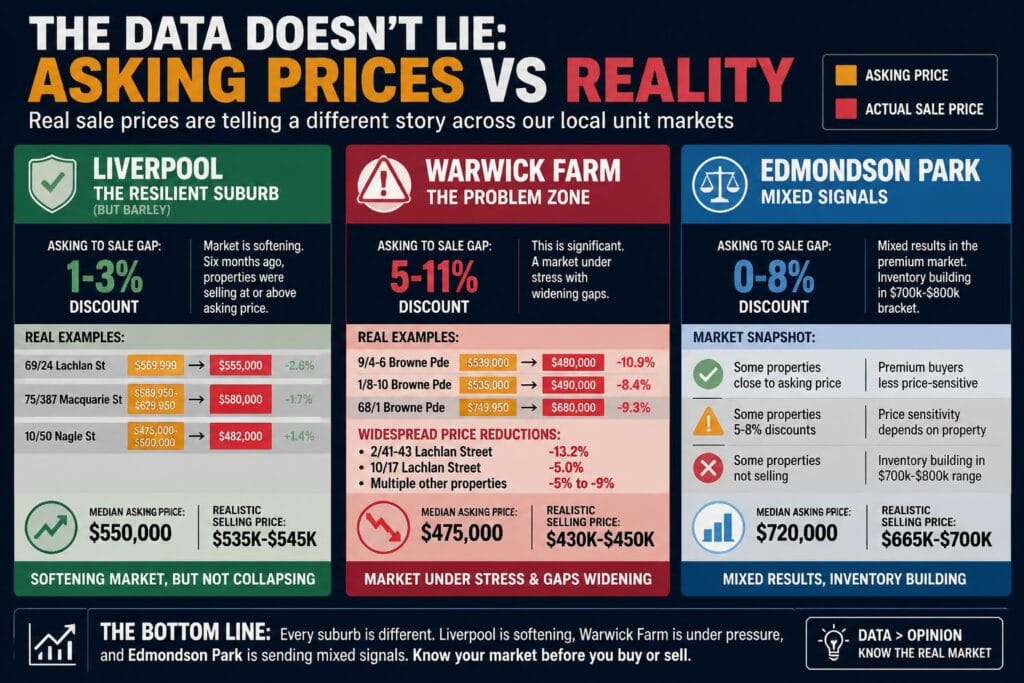

THE DATA DOESN’T LIE: ASKING PRICES VS REALITY

Here’s where it gets interesting. If you look at the current listings on realestate.com.au, you’ll see asking prices that look reasonable. But if you compare those asking prices to what properties are actually selling for, a different picture emerges.

Liverpool: The Resilient Suburb (But Barely)

In Liverpool, the gap between asking price and selling price is relatively modest – typically 1-3%. That sounds healthy, but it’s actually a sign of softening demand. Six months ago, properties in Liverpool were selling at or above asking price. Now they’re selling at a discount.

Real examples:

- 69/24 Lachlan Street: Asked $569,999 → Sold $555,000 (-2.6%)

- 75/387 Macquarie Street: Asked $589,950-$629,950 → Sold $580,000 (-1.7%)

- 10/50 Nagle Street: Asked $475,000-$500,000 → Sold $482,000 (+1.4%)

The median asking price in Liverpool is around $550,000. The realistic selling price? Probably $535,000-$545,000. That’s a softening market, but it’s not collapsing.

Warwick Farm: The Problem Zone

This is where things get serious. Warwick Farm is showing asking-to-sale price gaps of 5-11%. That’s not normal market friction – that’s a market under stress.

Real examples:

- 9/4-6 Browne Parade: Asked $539,000 → Sold $480,000 (-10.9%)

- 1/8-10 Browne Parade: Asked $535,000 → Sold $490,000 (-8.4%)

- 68/1 Browne Parade: Asked $749,950 → Sold $680,000 (-9.3%)

And it’s not just individual properties. We’re seeing systematic price reductions across the suburb:

- 2/41-43 Lachlan Street: -13.2% price reduction

- 10/17 Lachlan Street: -5.0% price reduction

- Multiple other properties showing 5-9% reductions

The median asking price in Warwick Farm is around $475,000. But realistic selling prices are probably $430,000-$450,000. That’s a 5-8% gap – and it’s widening.

Edmondson Park: Mixed Signals

The premium market is showing mixed results. Some properties are selling close to asking price (the premium buyer isn’t as price-sensitive). Others are showing 5-8% discounts. And some aren’t selling at all – inventory is building up in the $700-800,000 bracket.

WHAT THIS MEANS FOR DIFFERENT BUYERS

First-Time Buyers

If you’re a first-time buyer, Warwick Farm is actually looking interesting right now – despite (or because of) the price falls. You’ve got negotiating power. Sellers are motivated. Properties are sitting on the market long enough that you can be selective. The risk is that prices keep falling and you buy into a declining market. But if you’re planning to live there for 5-10 years, that risk is manageable.

Liverpool is also worth considering, but you’ll have less negotiating power. Prices are holding up better, which is good news if you’re buying for the long term, but it also means you’re paying a premium relative to Warwick Farm.

Investors

This is where it gets tricky. The yield story in Warwick Farm has been compressed by falling prices and stagnant rents. The capital growth story is uncertain. The CGT changes are making the tax efficiency argument weaker. Honestly? I’d be cautious about new investment in Warwick Farm right now. Wait for the market to stabilise.

Liverpool is slightly better positioned, but only slightly. The yields are still modest (around 5.3% gross), and capital growth is uncertain.

Edmondson Park is the premium play – you’re betting on capital growth, not yield. That might work out, but it’s a different investment thesis.

Downsizers

If you’re downsizing from a house to a unit, Edmondson Park is still the best choice. You get modern amenities, better supply constraints, and a different buyer demographic. Liverpool and Warwick Farm are more “investment” suburbs than “lifestyle” suburbs.

WHAT THIS MEANS FOR SELLERS: THE HARD TRUTH

Now, let’s talk about the elephant in the room – if you’re a seller right now, you’re facing some difficult choices.

The reality is this: the market has shifted decisively in favour of buyers. Asking prices don’t matter anymore. What matters is what buyers are willing to pay. And right now, they’re willing to pay 5-13% less than asking in Warwick Farm, and 1-3% less in Liverpool.

You’ve got two paths forward:

Path 1: You Have to Sell Right Now

If you must sell immediately – whether it’s due to personal circumstances, financial pressure, or investment strategy – then you need to be strategic about how you approach it.

First, select an agent that specialises in negotiation and marketing. This is not the time to use a generalist agent, a friend of a friend or someone who relies on “traditional” sales methods. You need someone who understands how to craft a captivating campaign that protects your sales price in a buyer’s market.

What does this look like? It means:

- Professional photography and videography that showcases the property’s best features –

- Targeted digital marketing that reaches motivated buyers before they see your property listed at a discount elsewhere

- Skilled negotiation tactics that help you extract maximum value from buyer offers

- Strategic pricing that’s realistic but doesn’t leave money on the table

- Effective communication that emphasises the property’s strengths and differentiators

The agent you choose should have a track record of achieving sales prices close to asking in this market. Ask for evidence. Look at their recent sales. Check the asking-to-sale ratios. If they’re consistently achieving 95%+ of asking price in this market, they’re the right person to talk to.

If you have any questions about selecting an agent or would like further information then please contact me directly, alternatively you can book an in home appraisal at your convenience.

Path 2: You Can Wait for the Dust to Settle (Preferred)

It might sound strange for a Real Estate agent who is motivated in selling a unit in Liverpool to say “hold off”, but I think before you start calling out the real estate agents to sell your unit in Liverpool that you should strongly consider:

Real estate moves in cycles: Like any market like gold, shares, oil etc. The price moves up and down based on many factors, and we have highlighted in this article the four we believe are moving price the moment. The real estate market has run well for a long time and like any good market it needs to correct. The great news is that corrections usually don’t last that long and while we can never make guarantee’s on what a market will do, we can see what happened previously….

Your Price and potenital negative equity: Homeowners only need to worry about price on two days. The day they settle and the day they sell. Any other day is realisitcally that day or month or year. The media and dare I say it, us real estate agents, make much more of it than we should. Consider? yes, but take action without speaking to experts? , I wouldn’t, and I have never sold one of my own properties that I didn’t have a great reason for…its just that simple.

Liverpool and Fairifeld are Growing: Yes put everything else aside, Liverpool and Fairfield are growing. The new airport in Western Sydney opens soon, Amazon, Wharehousing, datacentres…Alot happening around us at the moment and some great employment opportunities for the City of Liverpool and Fairifeld. Public transport needs a push along but overall the new M12 and many upgrades are now becoming more than just talk, things are a little exciting out here, so why would buyers not look to make the move to more affordable markets of Liverpool and Fairfield to live?

Cost of Material: And this one is a big one. The cost of one single brick that makes up your home….isnt falling….and he cement to hold the brick in place is also not dropping in price. Building homes, costs “what it costs” and while improvements might be made, the cost of rebuilding + your land assessment notice is a great way to get real about prices quickly in a falling market. Many homes would cost a great deal more to rebuild today by earnings standards.

The key question is: can you afford to wait? If you can, it’s worth considering.

We got the 1–3% growth forecast wrong. Spectacularly, embarrassingly wrong. But the data we’re seeing now is clear: the Liverpool unit market is under stress, Warwick Farm is under serious stress, and Edmondson Park is showing cracks.

The perfect storm of CGT changes, inflation, petrol prices, and RBA rate hikes has created a buyer’s market in most segments. Negotiating power has shifted decisively to buyers. And prices are falling – particularly in the segments where supply is highest and demand is weakest.

What happens next depends on whether the RBA cuts rates, whether the CGT changes become law, and whether the broader economy stabilises. But for now, the trend is clear: 2026 is not the year of 1–3% growth. It’s the year of market correction.

And if you’re thinking about buying or selling in Liverpool, Warwick Farm, or Edmondson Park, the data suggests you should move carefully. The market is moving fast, and the opportunities are real – but so are the risks.

Disclaimer: This analysis is based on transaction data current as of 27 June 2026 and market listings as of the same date. Property markets are inherently unpredictable, and forecasts are subject to significant uncertainty. The author’s previous 1–3% growth forecast proved incorrect, demonstrating the limitations of market prediction. Readers should conduct their own due diligence and seek professional advice before making property investment decisions. https://www.gregory.agency/privacy-policy/